Sunday 23 February 2025

In recent years I have joked in presentations that if I had £5 for every report or article I have read on the barriers to improving energy efficiency I could retire. It is a topic that has received a lot of attention, with some good and some not so good analyses. As part of my series of extracts / blogs inspired by my 1985 PhD this one reproduces what I wrote about barriers back then. As with the other PhD blogs you have to translate ‘energy conservation’ as ‘energy efficiency’, but other than that many of the same issues still appear in organisations. Key take aways include: failures of information and communication; failures to make energy efficiency options explicit; failures to think strategically and link energy efficiency decisions to wider corporate investment decisions, the importance of putting responsibility for energy efficiency in the hands of operational management and not just relying on engineering or technical teams, failure of senior management to understand technology, the power of paradigms and belief structures based on previous experience, and the importance of ‘champions’ questioning decisions.

The piece has had light editing from the 1985 original.

BARRIERS TO INVESTMENT IN ENERGY CONSERVATION

The barriers to energy conservation investment can be divided into two categories:

(a) techno-economic

(b) managerial

The term techno-economic is used as there are rarely purely technical barriers to applying existing equipment, the problems come when technical factors cause failure to meet the required economic return, hence preventing investment. Managerial barriers include all aspects of management that prevent investment in profitable opportunities.

It was stressed earlier that the profitability of energy conservation techniques is sensitive to site specific factors, and the importance of site specific factors should not be discounted.

The majority of this section is concerned with managerial barriers because of the site specificness of profitability. Without some form of energy management activity the profitability of techniques will not even be evaluated and so it is considered that managerial barriers are more important than economic barriers. The soft systems model of management activities necessary in energy management (also referred to here) is used to explore examples of different categories of management problems discovered in the sampled companies and in the literature.

TECHO-ECONOMIC BARRIERS

The 1985 discussion of techno-economic barriers focused on the economics of various measures including: industrial heat pumps, (which were having a resurgence in the early 1980s), Combined Heat and Power, sub-metering, energy management systems, and low energy lighting, amongst others. Given the changes in technology availability and prices this section remains just of historical interest and so is not reproduced here.

MANAGERIAL BARRIERS

Introduction

The following sections explore managerial barriers to energy conservation. Many reports on the barriers to energy conservation cite management problems but do not explore them in detail. Here the soft systems model of the activities necessary in energy management is used to examine barriers to energy conservation. The examples used are drawn mainly from the interviewed companies with some from the literature. Three types of managerial barriers can be distinguished: informational, strategic, and organisational and human. Each is now discussed in turn and the interactions between the three types described.

Informational Problems

Probably the biggest barrier to energy conservation is lack of information, or poor information management of one kind or another. As shown in Section One, 26 companies out of 49 sampled in the brewing sector monitor energy consumption at greater than monthly intervals or not at all. Without regular management information, effective action is unlikely to occur as shown by the evidence of these companies, eleven of which reported no reduction in specific energy use over the last two or five years.

In the dairy sector sample, two out of twelve sites did not monitor energy use at all while in the malting and distilling sectors samples monitoring is nearly universal. The incidence of monitoring in the four sectors was higher than that reported by Hoare (1983) in a geographically localised but general in industry sector, survey in which only 50% of respondent companies practiced some form of energy monitoring. We have seen that most sites in the brewery and dairy sectors do not adjust their monitoring figures for variances such as production, production mix, season and climate. Corrections are more often made in the distilling and malting sectors. Only twelve out of 49 sites in the brewing sector divide energy use into cost centres and allocate responsibility for energy to line managers, while only two out of eight dairy sites do. In the other sites engineers are responsible for energy conservation.

In two distilling companies production managers are responsible for energy and all other resource uses, energy specialists provide a service to the production managers. In the other distilling companies and in malting sites, the energy manager, usually an engineer, is responsible for energy conservation. This allocation of responsibility is necessitated by a lack of information on energy use within the plant. Provision of this information requires sub-metering which generally does not exist. Giving responsibility for energy conservation to engineers can create organisational barriers to change which are discussed in more detail below.

Another informational problem, possibly caused by organisational and human problems, occurs when information is either not passed on to the relevant people or when people do not understand the significance of information. In one of the large breweries interviewed it was admitted that prior to a recent management “shake-up” information concerning energy use was collected but not distributed to any managers. Roberts (1983b) cites a similar case in a brewery in which after the information was circulated it quickly led to action that saved one-third-of the energy used in bottling.

In one distillery interviewed the chemistry laboratories were responsible for carrying out boiler blow-down water and stack gas analyses. When the readings were outside set limits (indicating low efficiency that can easily be corrected), the chemist often did not communicate the message to the chief engineer as he had neither been trained to understand their significance, nor to realise his own role in the communication chain of management.

Another major problem which is information related, is the existence and prevalence of paradigms. All too often decisions appear to be based on paradigms and views that may have been relevant in the past but have become out of date. One of the quickest and cheapest ways to save energy is simply to question all practices and assumptions. Roberts (1983b) cites the case of a brewery where the same product was being stored in three separate vessels at three different temperatures, 30°F, 38°F, and 44°F respectively. In each case, the product was bottled and delivered under the same name and tested against a common quality standard. A detailed investigation led to a more rational and lower overall consumption of energy, and revealed spare refrigeration capacity in each case.

In one brewery the author discovered that a heat exchanger was working in reverse most of the time, heating up effluent instead of recovering heat from it before dumping it to drain. Similar examples abound in companies with extensive energy management programmes. An interesting example of a paradigm concerns pumps, again in a brewery. The type of pump used was inefficient because of its impellor design but preferred by the brewers as it was “easier to clean” than the alternative, more efficient pump. Only after extensive tests and persuasive efforts did the brewers admit that it was just as easy to clean the more efficient impellor. Of course the threat of biological contamination in a brewery is serious but the brewers exhibited an almost fanatical unwillingness to even consider change. Belief in paradigms, and failure to question assumptions represents a failure to see the problem and available techniques as they exist now. Several viable techniques are prevented in some cases because engineers distrust a technique they experienced ten or twenty years before, ignoring any advances in knowledge and ability made in the intervening period.

Strategic Problems

These can be divided into two types: lack of strategic thinking in integrating energy conservation investments and other investments; and lack of strategy within the energy conservation investment sub-set of company activities. The need to integrate energy conservation investment plans both with non-energy investments and with other energy investments was stressed in the soft systems model.

Examples of failures of the first type are now illustrated:

A small brewery invested over £2,000 on replacing a burner system for heating a copper. Savings were estimated before the investment at £1,000 p. a. and these were being achieved. Within a year however, the copper was replaced as part of the normal capital investment cycle. This illustrates a failure to think strategically about the effect of planned or anticipated changes to process equipment (or possibly the underlying process itself in some cases) on energy conservation investments. The company did learn from its mistake and ensured that energy saving features, including a novel heating system, were incorporated into the new copper. These reduced the gas bill by 20% relative to the performance with the improved burner system.

A medium sized brewery installed a CO2 recovery unit on the understanding that the alternative method of beer pushing, using nitrogen, would not be installed. The engineering department had previously lobbied for a nitrogen system because of the energy saving potential. This occurs because with a nitrogen system, nitrogen blanketing can be used to de-aerate the water used for diluting high strength brews rather than using steam heating followed by refrigeration (de-aerated water is used as the presence of air in the water imparts an undesirable metallic flavour to the product). The brewers, however, had flatly refused to consider nitrogen pushing. Less than a year after the CO2 recovery system was installed the brewers changed their mind and announced a switch to nitrogen pushing. The capital and time invested in the CO2 recovery was largely wasted by this change in policy. Although some CO2 recovery will still be practiced after nitrogen pushing is installed, the system is now unable to achieve a satisfactory rate of return.

A brewery decided to open a “brew pub”, a public house which brews beer on the premises.

The engineering department was instructed to complete the installation by a certain date. The engineers estimated that the design, build and installation would take twice as long as the available time. The time constraint left insufficient time to design in several energy saving measures. The sole objective of delivery by a fixed time over-rode all other concerns. Constraints in the building, notably space, meant that advance planning for later addition of energy conservation features was also not possible. Of course, in retrospect, if the entire project was successful it could be argued that this was an acceptable compromise.

A brewery that was investing £1.2 million in a new brew-house had the option of including copper vapour heat recovery (CVHR) using mechanical vapour recompression (MVR). This novel scheme would have added £O. 5 million to the capital cost (before a government grant of 25%) and had a 2.5 year payback period which was within the company’s normal criteria for retrofit investments. The MVR system would have reduced brew-house running costs by 80%. The option was rejected by senior management on grounds of shortage of capital. Leasing the MVR system, a possible way round the capital constraint, was not considered by the company. A secondary reason, which if it goes ahead within a medium timescale would make this an example of systematic thinking, was a Board directive to reduce boil-off from 10% to 5% within ten years. This would reduce the cost-effectiveness of the MVR system. In this example the engineer was being systematic in trying to incorporate a major energy saving technique into a new brew-house necessitated by the normal capital investment cycle. If the reduced boil-off decision is implemented it may well show strategic decision making by the Board. It appears however that the interactions between the projects, for example the effects of reduced boil-off on MVR system size and return, were not considered.

A large dairy was built for a group and reputed to be the most modern in Europe in terms of automation at that time, but had a very low energy efficiency. With prevailing energy prices numerous viable energy saving projects were feasible. These would have been relatively easy to include during the design stage but “no attention” was paid to energy. The dairy was over rapidly designed and built with no attention paid to reducing energy costs. Staff at the dairy are now attempting to rectify some of the failures to incorporate energy conservation projects. Some retrofit opportunities have been made difficult or non-viable because of constraints built into the dairy. Consequently the dairy is locked into a higher energy consumption and higher running costs than could have been achieved even with techniques economic at the time of design.

Examples of good strategic, total system thinking in which the synergy between general investment decisions and energy conservation investments was considered include the following:

A medium sized brewery, when building a cask-conditioned beer line, included drainage sumps that would enable an effluent heat recovery scheme to be added later, even though this project was not past the idea stage. Without the drainage sumps, easily incorporated at the construction stage, the costs of adapting the plant for effluent heat recovery at a later stage would have been prohibitive.

Two small breweries, neither of which could allocate capital to retrofit measures, ensured that all new plant was designed to be energy efficient. In one company the Head Brewer even included meters in new capital plant expenditure, “hiding” them from the cost-conscious Board. This example could represent one of two possible cases. Either top management were being systematic and conserving capital for other, higher return projects, e. g. marketing, and the production manager (Head Brewer) was wasting capital on meters; or he was being systematic in using the opportunity afforded by new plant purchase and doing what he could against higher opposition. The important point is that this issue was not made explicit. Discussions with management suggested that sufficient capital was available for metering and that top management had failed to appreciate the importance of metering in reducing energy costs. This lack of appreciation indicates an important communication failure between energy managers, meter suppliers, government agencies and senior management.

Examples of the more narrowly drawn sub-system approach within energy conservation investment are now given:

A company operating high temperature kilns (not in the food, drink and tobacco sector) decided to install a secondary recuperator on one kiln. During the system design it was also decided to install a microprocessor temperature control system which would save energy by keeping the kiln temperature within tighter limits. The secondary recuperator was installed followed by the control system. The tighter temperature control reduced the exhaust temperature such that the temperature in the secondary recuperator fell below the dew point, consequently acid condensed out of the exhaust and rapidly corroded the recuperator. Better strategic design would have delayed the recuperator until the control system was in place and working. Then the design of the recuperator could have taken the lower temperature into account.

A company installed insulation behind a false ceiling without realising that uninsulated heating ducts passed through the void space. Consequently the heating bills increased because of greater heat losses from the ducts and they had to be insulated. Total capital costs would have been much lower if both the ceiling and ducts had been insulated at the same time.

An example of the problem of deciding when to invest in new techniques is the case of a large brewery which invested £50,000 in a computerised data logging system for energy monitoring in 1981. When the system was installed the company had an energy management system in which the engineering department was totally responsible for energy conservation. Within two years the data logging system was found to be inflexible and have insufficient monitoring points even for the existing organisational form. it was decided to switch to an organisational system in which line managers were responsible for energy conservation, (generally proven to be the most effective option). The data logging system had to be replaced by a more flexible and extended system.

This example shows the relationship between informational systems and organisational form (to be explored below) as well as the problem of when to buy new technology. Although it failed to recoup the investment the original system did help to sell the value of metering and monitoring to senior management. As Rosenberg (1982) and Jacques (1981) have shown, there can be rational reasons for not investing in new technology now and waiting for a more advanced, possibly more proven, and possibly cheaper form of the technology. This decision, however, must be made explicit. Costs and capabilities of electronic energy management systems in particular, in common with other electronic equipment, have rapidly changed during recent years.

We have seen that examples of non-strategic thinking leading to wasteful investment occurred in a variety of companies, of all sizes. Some of the companies were noted for successes in energy conservation. Examples of both good and bad strategic thinking sometimes occurred in the same company. In all cases returns from investments were reduced, if not obviated. Several problems appear to be due to a lack of appreciation of technological problems by top management. Although working under pressure does have advantages the example of the brew-pub is extreme. Essentially the project had to be “crashed”. If the extra costs, capital, running and human costs, were considered explicitly and judged to be less than the benefits the decision would be defensible. If, as seems likely, they were not, it was a poor decision. In either case the impression gained is a lack of appreciation of technical problems. The example of the new dairy is similar and possibly reflects poor production facility planning at a higher level.

The example of nitrogen pushing and the CO2 recovery unit suggests a lack of any consistent, explicit technology policy. The Head Brewer’s initial. rejection of nitrogen pushing was reversed within a year, suggesting that either the original decision, was ill-considered, or the degree of uncertainty in this “decision” was not correctly communicated to engineering staff and others. The policy was understood to be “no N2 pushing” whereas it seemed in retrospect to be “wait and see”. If this had been explicitly recognised by all parties the CO2 recovery system could have been delayed.

Several brewery engineers complain that top management, which is often dominated by marketing and accounting specialists, do not understand technology. It would be easy to dismiss this view but some of the examples do support it. Top management decisions with technological implications often appear to be made without recognition of these implications and without strategic technological planning. The need for such planning and general acknowledgement that senior management lack technological know-how is found in Pappas (1984) and Steele (1983).

Other examples also suggest that top management do not understand technology. One brewery engineer was asked whether he could use mild steel trunking instead of stainless steel on a boiler economiser to reduce capital costs. This would have been possible but the estimated lifetime of the ducting would be less than two years. The project had a payback period, with stainless steel trunking, of about two years. The engineer resisted and won the case. The need for systematic planning at all levels is again illustrated by this case. If senior management had alternative higher return projects in which to invest they were correct to try to reduce capital costs. Their lack of technological know-how led them, however, to do this in the wrong way. Delaying the economiser rather than trying to impose false economies would have been a better strategy. This attempt implicitly shows a lack of faith in the engineer’s ability to design or specify an appropriate system. If senior management did not have alternative projects they did not have a valid reason to reduce capital costs. The important point again is failure to make this issue explicit. Many brewery managements have problems understanding technology. In the words of one brewery engineer, “this place has gone through a technological revolution and no one has adjusted yet”. The revolution appears to have been more accidental than managed. The brewing industry in particular remains saddled with an unwarranted craft romanticism whereas the reality is a high technology, chemical engineering operation.

The nature of energy conservation activities, and technology in general, suggests that an explicit technology policy, if not an energy policy, is necessary. Only one example of an explicit energy policy was found within the four sectors examined. This contrasts with experience in the chemical industry (S R Graham, D Boland, personal communications).

Some examples of non-strategic thinking are a result of day-to-day pressures taking precedence. One brewery engineer said that the only time he had to work on projects was in the evenings and at weekends. Although such application is laudable it is a comment on the organisation in which such “moonlighting” is necessary. The day-to-day pressures seem to have three possible causes: poor management; pressure caused by projects being given priority by top management; and organisational designs and climates in which engineering staff are interrupted throughout the day on minor administrative matters (a case of confusing the urgent with the important). These causes reflect hierarchical structure problems of the firms’ management which have effects other than in energy management activities. These are specific examples of the general disease of bad management.

Organisational and Human problems

In most of the sites in the four sectors large enough to merit separate engineering departments responsibility for energy conservation was primarily with the engineering function. Engineers have technical expertise in energy related matters, (though not usually energy conservation per se), but only utility generation in boiler houses, and possibly energy distribution is under their direct control. Energy use, or mis-use, is under the control of the users and not the producers. This important principle is often ignored. Any attempt to make energy management at the good housekeeping level the responsibility of engineering staff is likely to lead to several problems. Firstly the engineer-energy manager is unlikely to have time to keep a close check on all energy users in all departments. Secondly, any attempt to change working habits in another manager’s department is likely to compromise that manager’s authority. Thirdly, without explicit responsibility the department manager is unlikely to have sufficient motivation to ensure good housekeeping is practiced.

One remedial approach encountered is to appoint energy wardens who are made responsible for ensuring good housekeeping in their particular areas. This may be good for spotting problems such as steam leaks but is unlikely to result in operational changes where appropriate because the energy wardens lack authority. In some brewing sites where the engineers are responsible for energy conservation a common attitude amongst line managers is that “energy is something the engineers look after”. These managers have no explicit responsibility for controlling energy costs and express their objectives as producing beer, not producing beer at a profit. In two sites where this occurs there are suggestion-schemes and energy committees but 80% of the input comes from the engineering

departments.

It is likely that that line managers have insufficient expertise in energy conservation. Most managers, however, do have an in-depth knowledge of their own production equipment and operations that should be a good basis for energy conservation activity. It seems more likely that the lack of action is caused by a lack of motivation. Unless departments or areas are sub-metered and line managers given full explicit responsibility for reducing energy costs, in co-operation with engineers, there is no motivation. The effect that this problem can have is illustrated by the example of a production manager who had always scheduled steam cleaning of plant at weekends. This resulted in the boiler having to be fired up at weekends at an estimated cost of £600 per occasion. On one weekend when essential maintenance work necessitated a complete electrical and therefore steam shut-down, (the boilers cannot be run without electrical power), the cleaning operations were rescheduled to occur during the week.

When the plant energy manager suggested that this could be done every week, saving about £30,000 per annum, the production manager refused. The energy manager subsequently arranged several notional electrical shut-downs at weekends to illustrate that rearranging the cleaning was possible and resulted in little, if any, extra cost. After several “shut-downs” and persistent persuasion by the energy manager, the practice was made permanent. The production managers stated reason for refusing to reschedule cleaning operations, extra cost. was not justified. If the costs had been real the energy manager would have been wrong to persist and this would have reflected unsystematic thinking on his part. In this case however, he did consider all other costs and decided upon action which was subsequently proved correct. The production manager did not regard energy conservation as part of his role. Presumably, he felt no motivation to do so because energy use in his area was not metered and he was not explicitly made responsible for energy use within the area.

The importance of allocating responsibility to line managers is supported by Roberts (1983b) and Boatfield (1982). The latter stresses that line managers must be totally responsible for all functions including engineering. In order to be responsible for a technical function, the non-specialist must make the engineering management accountable to him for the engineering function. The same applies to other specialist functions such as Health and Safety. This approach has had spectacular results, both in energy conservation and environmental pollution control (Boatfield, 1982; see also Financial Times, 29 August 1980).

One distillery company illustrates the difficulties in switching to a system in which line managers are given full responsibility. The group energy manager realised the problems inherent in having chief engineers responsible for controlling energy consumption. Despite having one supporter on the main board it took two years to change the system. Eventually, in 1981, the Assistant Manager at each site was appointed as an Energy Co-ordinator. Each had complete responsibility for energy conservation and engineering staff as a resource. Energy savings since 1981 have been about 25%. The central energy manager, a chemical engineer by training, believes that technical people are needed for energy work but they do not need to be energy engineers: “there is no problem in a technically aware-person acquiring the principles of energy conservation”.

Organisational problems can also occur at the level of new equipment purchase. In a large brewery where the manager responsible for energy use in public houses, an engineer, was establishing specifications for new buildings and renovations, encompassing lighting, heating and ventilating, cooking and dishwashing equipment. The purchasing department had traditionally been responsible for purchasing new equipment and its objective had often been to minimise capital outlay. The energy manager was trying to minimise running costs within a definition of profitable investment (i. e. the payback period criterion). There are, however, no formal links between purchasing and the energy management function. The energy manager is having to forge these links but is encountering resistance from the purchasing department, who see a takeover of some of their functions.

Another “human” problem, possibly exacerbated by organisational designs in which engineers are given responsibility for energy conservation, is excessive concentration on hardware and high cost solutions. Roberts (1983b) cites a case where high cost measures were instigated first and saved £250,000 a year on a site having an annual fuel bill of £4 million. The capital cost of the projects amounted to £250,000 and management were pleased with achieving a one year payback. Later, when the site was examined for no-cost and low-cost improvements, a further £250,000 per annum of energy was saved for a capital cost of only £25,000. All too often engineers concentrate on hardware instead of information and organisational software.

An organisation in which functions are rigidly separated can present barriers to effective energy management. In many companies interviewed, engineers produced proposals on a payback basis which were then handed to accountants for DCF analysis. If any sensitivity analysis is conducted it is done without access to engineering information necessary to assess technical risks. This rigid separation of functions lowers the usefulness of sensitivity analysis. In one case found the project had been rejected because of a low IRR but a check by an engineer trained in DCF techniques proved the analysis was incorrect. In one of the larger breweries engineers had recently acquired microcomputers and started to do their own DCF calculations and spreadsheet modelling. Only one company in the brewing sector sample had a separate energy conservation capital budget, expenditure being requested from a general capital budget. This means that projects can be accepted and rejected on a piecemeal basis, making integrated planning of projects more difficult. It also has two important consequences for companies supplying energy saving equipment. Firstly, as in all marketing, it is important to find out at an early stage in the contact who actually makes the decision. In most cases the engineer or energy manager decides what equipment or service he requires, but the finance department has the final say over what is bought through control over the capital budget as well as financial appraisal. In such cases it is important that the potential supplier finds out (a) what the capital expenditure criteria are; and (b) what the preferred methods of proposal presentation (i. e. IRR, NPV, with/without tax etc) are, so that it can either help the engineer prepare, or itself prepare, a proposal with a high probability of acceptance. These basic actions seem to be overlooked by many supplying companies.

The second and possibly more serious consequence is that engineers prepare proposals on the basis of quotes. Proposals are then passed on to finance departments. If they are accepted they are then put into the following year’s capital budget. This can result in long delays between acceptance and implementation with obvious consequences for suppliers’ cash flows. The establishment of a separate energy conservation capital budget aids the integration of projects through formation of a portfolio and can reduce the time lag between project acceptance and implementation.

SUMMARY

Managerial barriers to energy conservation investment have been categorised into three related types: informational, strategic and organisational and human. The most important informational barrier, and probably the most important barrier of all, is failure to monitor energy use and costs. Monitoring is linked to organisational barriers. Organisations in which energy managers are responsible for controlling energy costs often encounter problems of lack of coordination and lack of motivation for line managers. Giving full responsibility to line managers, and a coordinating and support role to energy “managers”, induces this motivation. To do this, however, requires a well developed monitoring system which breaks down energy costs and usages into cost centres and delivers relevant and timely information in a usable form to line managers.

Another informational problem is the existence and prevalence of paradigms both about existing production equipment and energy conservation techniques. These reflect a failure to understand available techniques as they exist now and unwillingness to experiment in a scientific manner. These managerial barriers conspire to prevent investment in energy conservation techniques, even where such investment would if properly evaluated, meet the company’s investment criteria.

_____________________________________________________________________________________

REFERENCES

Hoare, A.D. (1983) Energy management on Tyneside: a survey. Paper presented at Tyneside Energy Day Conference, 12 January 1983.

Roberts, M.C. (1983b) Energetic ways to cut costs. Management Today, May 1983

Pappas, C. (1984) Strategic management of technology. Jnl. of Product Innovation Management, Vol. 1,1984

Steele, L. (1983) Mangers’ misconceptions about technology. Harvard Business Review, 61. November-December 133-140Boatfield (1982)

Boarfield, D.W. (1982) Energy environmental equation. Paper available from D.W. Boatfield, Manager, Energy Environmental

Financial Times 29 August 1980

Photos taken on my tour of whisky distilleries in the summer of 2024

Saturday 15 February 2025

The latest in a series of pieces derived from my 1985 PhD.

We often talk about adopting technology, but for all but the simplest of technologies the process is usually one of adaptation. Adaptation requires site specific engineering, the kind of engineering that is unspectacular but essential. Numerous site specific factors drive costs as well as savings, and therefore the economic viability, of any proposed measure. Therefore you cannot assume that a technology that works in one site will work in another site that is in the same sector, or even another site that is ostensibly similar.

The technologies referred to have moved on, (the original did not refer to LEDs but rather compact fluorescents so I have updated that), and the innovation literature references have probably been superceded but the principles remain the same. The fact that a company has not adopted an energy efficiency measure, does not indicate ‘sloth, bias or stupidity’ – even when the technology is regarded as a ‘no brainer’ or ‘low hanging fruit’. In addition, of course, different companies may have different financial criteria for their investments driven by factors such as differing economic performance, financial structure, strategy, shareholder preferences or management approach.

Adoption versus adaptation

In many studies the purchase of technology is often presented as a simple adoption process. In most, if not all, energy efficiency investments, (as well as other areas of technology), the process is more one of adaptation. Even when a concept is well proven and the basic hardware exists some adaptation work is necessary for all but the simplest technologies, to make a viable system in the particular site in question. This requires original, though not dramatic, engineering design work. The basic hardware may well be standard and simple but the system must be engineered to meet the technical conditions and the required economic return at each specific site. The difficulties this can present, and the effect of site specific technical factors on economic viability, have been neglected in the adoption literature.

There is a great variety of energy efficiency technologies available, ranging from LED lamps to sophisticated process heat recovery and electronic energy management systems. Each technique has a degree of adaptability, the inverse of which can be labelled specificity. At one end of the scale, with a high adaptability, would be LEDs which can plug straight into existing fittings. In more complex relighting situations, such as a warehouse where high pressure sodium lamps are to replace fluorescent tubes, considerable adaptation of the existing lighting circuits may be necessary.

A technique with a lower adaptability than low energy lighting would be heat recovery from boiler stacks using economisers. Ostensibly this mature technology (first patented in 1845) looks very adaptable as it can, in principle, i.e. technically, be applied to any gas fired boiler, or dual fuel boiler if a bypass is used during oil firing. Numerous site specific factors affect the financial viability of proposals for boiler economisers, including:

- physical space for the hardware

- load bearing supports

- quantity and quality of demand for hot water

- flue gas temperature and-composition

- boiler utilisation

- boiler load pattern

- time spent burning gas (for dual fuel boilers).

Total system cost, as in other heat recovery projects, is often three times the cost of the economiser or heat exchanger. At two brewery and one dairy sites visited during the research, economisers were not financially viable because of lack of space in the boiler house. Obviously it would have been technically feasible to extend the boiler house but the cost would have been prohibitive. Consequently, the technical potential for energy saving through the use of economisers at these sites is unlikely to be exploited at current prices until a new boiler installation is necessary for other reasons. Applications of commercially available hardware are rarely prevented by purely technical problems but by failure to meet economic criteria.

Specificity

Towards the higher end of the specificity scale, i. e. the least adaptable, would be a process heat recovery system. The number of technical factors affecting financial viability will be substantially higher than a simple boiler economiser. The determinants of the adaptability are the sensitivities of capital costs and savings to variations in specific technical factors inherent in the technique and the site. The technique of heat recovery from malting kilns using air-to-air heat exchangers has a higher adaptability than say brewery effluent heat recovery systems because the technical factors that affect capital cost and savings, notably physical dimensions, air flow rates, temperatures, tend to be similar between sites. There are only a few basic designs of malting kilns.

On the other hand brewery effluent heat recovery systems have a low adaptability into other brewery sites because their viability is very sensitive to site specific factors such as plant layout and quantities and qualities of effluent (determined by the type and operating conditions of existing plant, as well as production levels and mix).

The importance of specificity is supported by several writers on innovation. Rosenberg (1982) stresses the importance of adaptation and the role of “unspectacular design and engineering activities“. He also notes that in the literature there is frequent preoccupation with what is technically spectacular rather than what is economically significant. Rosenberg also emphasises the importance of studies at the level of the individual firm. Rogers (1962) in discussing the adoption of innovations divides the “antecedents” to the innovation decision into two categories:

(1) perceived attributes of the innovation, and

(2) characteristics of the adopters.

Five attributes can be summarised for the first category:

- Relative advantage

- Compatability

- Complexity

- Trialability

- Observability.

Compatability, “the degree of fit of the innovation with existing norms and needs of potential users“, (Rogers, 1962), subsumes adaptability as well as other factors.

The importance of adaptability, or its inverse specificity (in connection with innovations) is also supported by Boylan (1977), who states:

“The number of firms in an industry which are potential adopters of an innovation, and the proportion of their output to which it might be applied, depends on the functional specificity of the innovation at successive stages of development as well as the range of relevant processes and products in individual plants. Hence, adoption rates cannot properly be compared with the total number of firms in, or the total output of, their common “industry” classification. Rather the progressively changing characteristics of the innovation in its various forms must be accompanied by changing measures of the array of economically feasible applications.”

Gold (1977) notes that it cannot be assumed that the expected benefits of an innovation are so clear that all potential adopters would assess them similarly or even that all potential adopters give serious consideration to the same innovations in any given period. Economic viability in one site does not automatically confer economic viability in a similar site because the costs of adopting the basic hardware into a system can make it not viable. This is true even assuming similar definitions of economic viability. Gold also suggests that:

“the criteria applied to the evaluation of available innovations may differ widely among firms, reflecting differences in their internal urgencies, resource availabilities and specialised expertise rather than deriving solely from the demonstrable benefits of the innovation itself.“

Gold goes on to state:

“Instead of assuming ignorance, sloth, bias or stupidity as the causes of (such) restrained rates of diffusion, it would be more helpful to make field studies of the actual considerations and evaluations responsible for the decisions made.”

Bradbury (1978) observed that technology:

“is not something that can be bought off the shelf or stored in a bank vault“.

Components of systems may be bought off the shelf but an input or knowledge – engineering – is necessary to design financially viable systems, even where the concept has been used elsewhere.

In conclusion

Understanding technological change and how we use and adopt technology is important for policy makers and practitioners. We should not forget the degree of ‘unspectacular’ engineering that is necessary to adapt technology to a specific situation, and we should not forget the importance of relatively small-scale, unspectacular (and often unseen), incremental technical change – particularly in an age where we tend to focus on large-scale, spectacular innovation. Over time the cumulative effect of incremental technical change can be greater than that of spectacular innovations.

_________________________________________________________________________________________

References

BOYLAN, MG (1977) Reported economic effects of technological change in Research, technological change, and economic analysis. ed. B Gold, Lexington Books, Lexington Mass.

BRADBURY, FR (1978) The Leverhulme Project at Stirling in technology transfer: implications for the Scottish Economy. TERU Discussion Paper No. 14, Proceedings of Conference held at the University of Stirling, 17 and 18 October 1978.

ROGERS, EM (1962) Diffusion of innovations. Free Press, New York

ROSENBERG, N (1982) Inside the black box: technology and economics. Cambridge University Press

Sunday 2 February 2025

On the 29th January EP co-hosted the Net Zero Finance Leadership Summit. This unique event, held in the Guildhall, was supported Under our Innovate UK (IUK) funded ‘Shift to Net Zero’ project, and brought together senior people from local authorities, financiers, investors, lenders and other stakeholders focused on increasing investment into local, systemic, place-based net zero projects.

The Shift to Net Zero project consortium is made up of EP, Ibex Earth, Kent County Council, Surrey County Council, Essex County Council, and Brighton & Hove City Council. The ideas behind it are developed from EP’s work over many years reviewing, and in some cases working on, examples from around the world where energy efficiency financing had successfully scaled. The project also builds on the various tools we had developed and deployed to help derisk and enable energy efficiency and net zero investment decisions including: the Investor Confidence Project Europe; the Energy Efficiency Financial Institutions Group’s Underwriting Toolkit; ESCO-in-a-box®; the EU Horizon funded CREATORS project tools for developing community energy projects; and the UNESCWA Toolkit for Energy Efficiency Financing Instruments for Buildings in the Arab Region. The idea for a dedicated Net Zero Delivery Vehicle, the NZDV, started with a small piece of work EP did for IUK at the end of 2021. Through 2022/23 further work on the idea was funded through the Greater South East Net Zero Hub and in 2023 IUK funded phase 1 of the Shift to Net Zero project in which EP, Ibex Earth, and the four local authorities identified potential investments of £46 billion and further developed the concept. That work led to the current project which is about building capacity and advancing the NZDV concept.

The aims of the Summit were:

1. to bring together local authorities and private capital – 2 groups that rarely come together and speak different languages

2. to increase knowledge and understanding of the Shift to Net Zero project

3. to advance EP’s proposed NZDV, a public-private vehicle designed to overcome the barriers to bringing in private capital to local place based NZ projects

Key take aways from the meeting were as follows:

1. the barriers are non-technical and are based around lack of capacity on both sides

2. addressing the problem requires a systems based approach, both technically and organisationally

3. local authorities and financial institutions are both committed to solving the problems to ensure more capital flows into these kind of systemic projects.

4. there is huge gap between what is often called pipeline and well developed bankable projects – much of what is called ‘pipeline’ is more aspiration than real pipeline

5. there is lack of capacity in local authorities to develop projects and access private capital.

The audience of c.80 were highly engaged throughout a packed programme of presentations and panels.

The Net Zero Delivery Vehicle is designed to be an equitable public-private partnership that brings together local authority project opportunities and capabilities, with private sector development expertise and some initial seed capital for development. It’s structure meets the needs of private investors and lenders, ensures good governance, enables the ability to aggregate projects to a scale that is meaningful for institutional investors, and satisfies public sector procurement rules. The next stage is to get seed funding to structure the entity with the initial founder local authorities (and other interested authorities) and start operations.

The Shift to Net Zero project has also launched a knowledge sharing platform which can be found on nzdv.co.uk

Later in the year the project will host a second meeting to move the NZDV forward. Any local authorities interested in participating in the NZDV should contact Leo Bedford at ep – leo.bedford@epgroup.com

Friday 31 January 2025

Technical change – change in the technology we use to do things – is all around us and essential to achieving energy and climate goals, as well as to economic growth but we don’t often think about the process of change. Improving energy efficiency is a continual process of technical change. How does it happen?

There are three necessary conditions that have to be met before a technical change will occur. These are:

1) a TECHNICAL CONCEPT must exist, capable of being developed to the stage of achieving

2) an ADVANTAGE over alternative technical concepts and the status quo

3) the CAPABILITY of developing 1) to the stage of delivering 2) must exist.

All three conditions have to occur simultaneously and in the same place. An important modification to this is that it is more the perception of advantage and capability rather than any absolute values that motivate a ‘coupling agent’ to bring all three together and force a technical change. The coupling agent fulfills an entrepreneurial role even though in most cases of technical change around energy efficiency he or she is unlikely to be the classic independent entrepreneur, but rather an employee of an established organisation. The coupling agent can be motivated by many things, including: profit, position and profile, desire to change things for the better – perhaps best summed up by J M Keynes’ phrase ‘animal spirits’.

The technical concept may be a brand new idea, a new combination of ideas (old and/or new) or an old idea not previously developed because of lack of advantage or capability. The ease with which the concept can be turned into a commercially viable installation depends on the extent to which components of the concept are already embodied in available hardware. If the central concept is already embodied in commercially available hardware, then adaptation to fit the specific site – engineering – will be necessary. If hardware has to be developed, as in the case of an entirely new concept, or invention, more research and development work is necessary. Thus, there are different levels of research, design and development. Depending on the state of the concept it may involve R&D in the traditional sense, “experimental design” or more mundane “routine engineering design”. Most energy efficiency measures should ‘only’ involve routine engineering design, there is usually no need to develop new technologies with all of the risk that entails.

The advantage is usually, in the case of industry, an economic advantage. It may be an advantage over alternative concepts or over the status quo. Some advantages such as improved quality control or working environment may harder to quantify economically but may be considered strategic to the organisation. Measures judged to be strategic, for instance improving a product, or improving public perception of the company, are more likely to implemented than simple cost saving measures. An exception to purely economic and strategic drivers would be technical changes that are required to meet regulations e.g. emissions control.

Capability to develop the technical concept to the stage of achieving the required advantage over alternative concepts or the status quo may exist in either the potential host or a supplying organisation, or of course a combination of these. For most energy efficiency investments the basic hardware will already exist and the necessary capability will be the capability of adapting the basic hardware to meet the potential host’s technical and financial needs, essentially engineering work. The greater the level of research, design and development necessary to bring the concept to the hardware stage, the more important, and more difficult, it is to assess the capability of vendor companies and the host company itself. Undertaking projects that require R&D adds a significant extra uncertainty to the investment decision. For most energy efficiency investments, there isn’t a need for basic R&D, and in fact for most organisations undertaking such work would be inappropriate and far too risky.

To sum up, technical change occurs when a coupling agent, brings together a technical concept, perceived advantage and capability to deliver the change and achieve the desired advantage. This coupling activity is essentially entrepreneurial in nature and requires human energy applying development skills.

Saturday 25 January 2025

The latest in a series of blogs inspired by my 1985 PhD

There have been many, many studies over the years discussing the potential for energy efficiency, in fact there are almost as many studies on potential as there are on the barriers to energy efficiency. As I sometimes joke, if I had ten pounds for each of those I could probably retire. However, very few of the studies on potential really define potential.

The question of what is the potential for energy efficiency, both the meaning and the quantum, was an important element of my research which set out to review the feasibility of achieving a low energy future. As the work progressed, it became obvious that potential, when used in anything other than its pure physical science meaning, is a ‘soft’ concept that needs to be defined. Leach et.al., in their “A Low Energy Strategy for the UK’, along with many other studies of potential made no effort to different types of potential.

Potential is not static, it is continually being altered by technological and economic developments – it is a dynamic just like reserves and resources of oil and gas. At any time, and in any particular site, and site specificness is very important, there are the following types of potential.

- There is a totally theoretical potential based on the laws of physics without any consideration of practical available technology.

- There is the potential for improving energy efficiency that derives from the physics of the process or installation using known concepts i.e. not magic, which is also a theoretical potential.

- A sub-set of this potential is the potential that can achieved by applying available, existing technology.

- This sub-set, at any one time, is further divided into potential that is economic and potential that is not economic.

It is the latter that is actionable by the firm. It can be defined as the potential resulting from those investment possibilities that:

- are capable of being developed and implemented by the host organisation (or householder) or vendor/supplier/contractor

- meet the financial criteria set by the organisation making the investment

- are appropriate in context i.e. other considerations at the time.

The schema of potentials can also be divided into that available from retro-fitting and that available from installing new plants or processes.

Obviously the size of the potential depends on judgements and decisions outside the usually accepted boundaries of energy management. Clearly two organisations operating similar facilities could have different investment criteria due to differing decisions on priorities for capital or differing return requirements by their owners, giving different potentials even if their underlying facilities are identical.

Furthermore, and overlaid on these potentials are the perceptions and performance of management. Differences in perceptions may come from two sources, differences in the quality of internal and external information flows, and differences in the selective perception of information by actors in the process. Internal information includes energy performance information but also other information about the wider business. External information includes many things including information on the availability of technology and hardware, and views on future energy prices. For example, in one site the possibility of a certain energy efficiency measure may not be perceived at all due to a lack of knowledge. In another similar site that particular measure may be considered unrealistic because of a prior bad experience. Such ‘biases’ are important in determining what is considered achievable and appropriate by management. Perceptions filter objective reality.

As prices and available technologies change, the potentials change. Thus any attempt to estimate or measure potential will always be fuzzy. A real measurement of potential requires blending detailed engineering work with management views and perspectives – sometimes called an Investment Grade Audit. Gathering this level of detail is an expensive exercise with an ephemeral result. It is only worthwhile going to the expense if management believe a measure is likely to be implementable and investable.

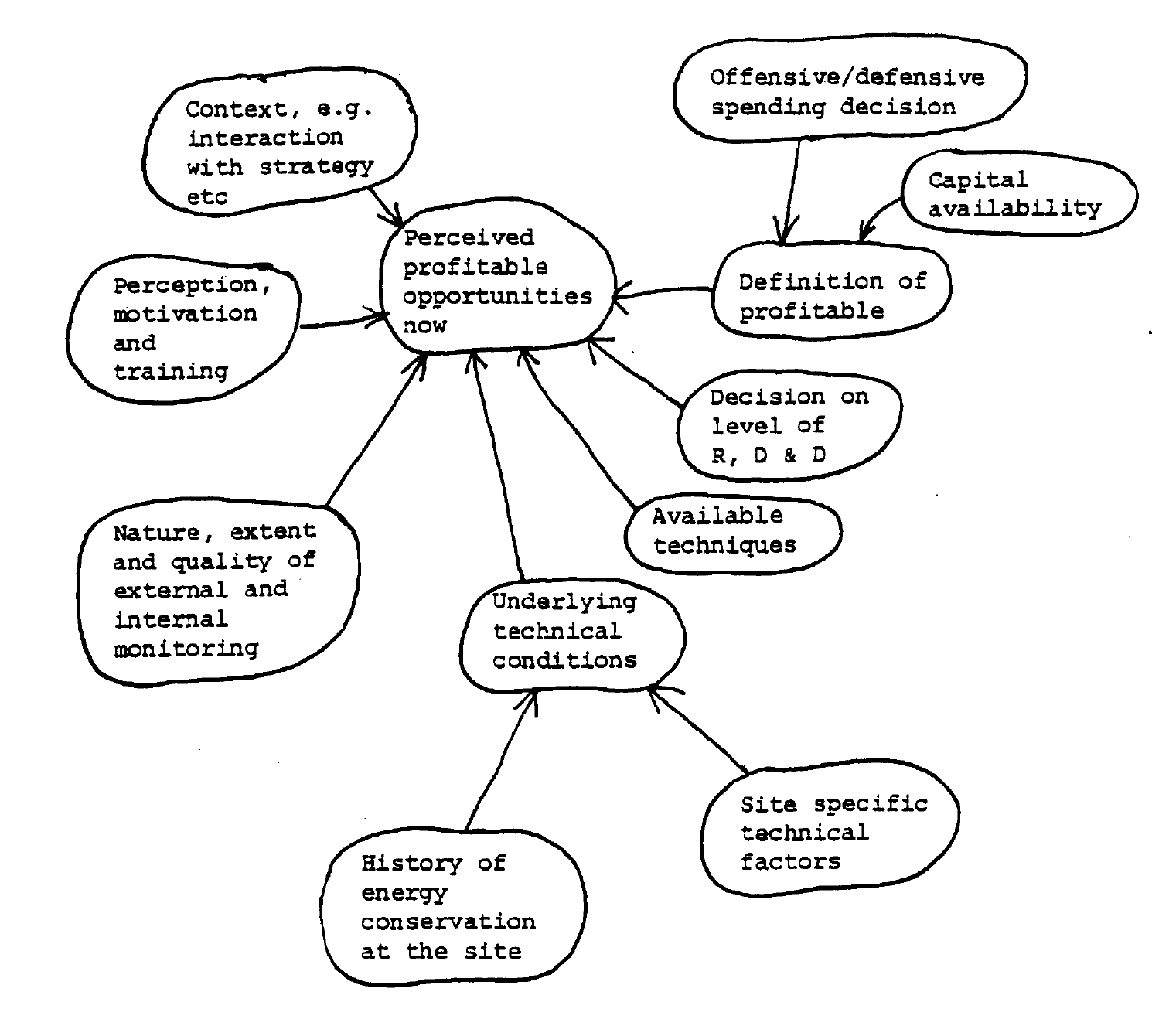

The factors that influence the potential in any one site at any point are shown in the soft systems inspired diagram.

This analysis emphasises the fact that potential for energy efficiency is analogous to that for energy resources and reserves, something that I explored in this 2015 blog, ’Energy Efficiency as a Resource’

The next time anyone talks about or writes about the potential for energy efficiency ask what is their definition of potential.

Dr Steven Fawkes

Welcome to my blog on energy efficiency and energy efficiency financing. The first question people ask is why my blog is called 'only eleven percent' - the answer is here. I look forward to engaging with you!

Get in touch

Tag cloud

Black & Veatch Building technologies Caludie Haignere China Climate co-benefits David Cameron E.On EDF EDF Pulse awards Emissions Energy Energy Bill Energy Efficiency Energy Efficiency Mission energy security Environment Europe FERC Finance Fusion Government Henri Proglio innovation Innovation Gateway investment in energy Investor Confidence Project Investors Jevons paradox M&V Management net zero new technology NorthWestern Energy Stakeholders Nuclear Prime Minister RBS renewables Research survey Technology uk energy policy US USA Wind farmsMy latest entries

- ‘Here we go again’ – but this time we have a choice

- The corruption of purpose in business – and how to address it

- Gee, I wish we could have a white Christmas, just like the old days….

- A look back at the last forty years of the energy transition and a look forward to the next forty years

- Domains of Power

- Ethical AI: or ‘Open the Pod Bay Doors HAL’

- ‘This is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning’