Thursday 21 September 2023

For the second day running I was speaking at an event, this time the Association of Decentralised Energy’s (ADE) annual conference. I had not spoken at the event for a few years and it is always a pleasure to work with the ADE. The topic of my presentation was metered efficiency and the Retrometer project which ep is involved with. Metered efficiency is a new paradigm which enables a number of things including; reducing the performance gap between what expected savings are and what actually occurs; pay for performance contracts which resemble Power Purchase Agreements and can be financed; time of day energy and carbon performance reporting; and allowing DNOs to see the effect of different efficiency measures and programmes on load curves. Information on Retrometer, which we hope will soon move forward into the Alpha phase with Strategic Innovation Fund support, can be found here and here.

Of course, there was much talk about the Prime Minister’s speech on net zero which rolled back previous commitments, and magically ‘cancelled’ policies which were not even under serious consideration. Some of the comments in the first panel which discussed the PM’s announcements got me thinking.

These included:

‘the beginning of undermining confidence in the independent Climate Change Committee’

‘policy weaponisation’

‘playing to people’s fears’

‘a political trap’

‘more US style politics than UK style politics’

Although my readers know me as an energy person, with a strong interest in space exploration and a love of David Bowie’s music, most people don’t know that one of my other great interests is American politics. I got into it through being interested in the space programme, (think JFK’s commitment to land men on the moon), got up in the early hours to watch Nixon’s resignation speech in 1974, worried through the Reagan years, and have studied it closely ever since. I have also seen the reality of US politics, at a local and state level, close-up and personal through a great friend in the Mid-West who became a politician. I am still not at liberty to tell some of the stories from that period. Of course the election of Trump was a terrible shock and I woke up nearly every day of his Presidency reading the news because I was so concerned about what he had said or done overnight.

So what is the connection between US politics and the PM’s announcement on net zero? Well, it is pretty clear that UK politics has been the subject to the same forces that resulted in Trump being elected, some internal but also clearly supported and amplified by very dangerous domestic and foreign actors. In some ways, these forces were more ‘successful’ in the UK than in the US (think BREXIT). People in the UK still under-estimate the danger represented by Trump, his supporters and MAGA ‘Republicans’. Make no mistake, they are authoritarian, anti-democratic and would undo decades of progress on issues such as civil rights, women’s rights and the environment, as well as potentially start a war. If you don’t see it this way you are not following closely enough. The 2024 US election is a critical decision point and whatever you may have read or believe about President Biden the choice is clear – it is between democracy and authoritarianism.

The common cry of the MAGAs is against ‘woke’ behaviour which in their view includes things like ESG investing and net zero. Their tactics include inciting fear about imagined slights like claiming that the Biden administration wants to ban gas stoves (ovens). This led Jim Jordan, a Trumpist Republican member of the House of Representatives to tweet: ‘God. Guns. Gas Stoves’. You can see the parallel with Rishi Sunak’s tweet saying: ‘We’re stopping heavy-handed measures: Taxes on eating meat. New taxes to discourage flying. Sorting your rubbish into seven separate bins. Compulsory car sharing. Expensive insulation upgrades.’ He also said: ‘We will never force anyone to rip out their old boiler for an expensive heat pump.’ None of these things were real policies.

So, I am not so worried about the impact on achieving net zero that the PM’s announcements yesterday will make. The momentum of investors, corporates and local governments is powerful enough to overcome these changes in policy on their own. What I am more worried about is the longer term and that this is another step towards more intense MAGA-style politics in the UK in which facts are ignored, (and even denigrated), conspiracy theories are promoted, and divisions are intensified by politicians driven by authoritarian and anti-democratic urges. If as the polls suggest Labour win the next election the Conservative party will most likely lurch further to the right and mount a long campaign based on ‘anti-woke’, anti-science positions and fighting ‘the blob’, equivalent to the MAGA’s opposition to the ‘Washington elites’. Hopefully these won’t resonate with the majority but there is a risk they could, particularly if there is an extended period of relative economic problems.

We do need to worry about how to get to net zero, but we really need to worry about the direction politics is taking, and how much worse it could get.

Wednesday 20 September 2023

It was a pleasure to attend the East of England Local Government Associations’ Net Zero conference on Wednesday. It was a well attended, wide ranging and informative event covering investment, design, transport and behaviour change. I was on a panel addressing the problem of how to attract investment to achieve net zero ambitions. I made the following remarks on the panel talking about investment, revisiting one of my common themes – how to bridge the development gap between ‘here’s a good idea’ and ‘here’s a high quality financeable project’.

Good morning, it’s a pleasure to be here in Cambridge addressing the important topic of achieving investment to deliver net zero ambitions. That is something that I, and the rest of the ep team spend a lot of time thinking about and working on.

It is clear that getting to net zero requires a huge amount of investment. It is true that behaviourial issues are important but fundamentally this transition is about investment – investment in transforming our infrastructure from being based on fossil fuels and combustion to renewable electricity and energy efficiency. It is on a scale equivalent to the industrial revolution, and when historians look back in a 100 years it will be seen like the industrial revolution.

So how much investment is needed? The Climate Change Committee say £50 billion a year up until 2050.

What is clear is that this level of investment cannot come from the public sector alone. We have to access institutional capital.

At the same time as we are addressing net zero within local government and companies, we are seeing a revolution in finance, one in which the finance sector is being driven by regulation and customer pressure to invest in a more sustainable way. We see this in things like the EU Taxonomy and TCFD forcing financial institutions to look at climate related risks. Just like businesses and local governments, the financial institutions are trying to work out how to make the transition towards net zero. You can be cynical, and probably should be cynical, about some of it because ‘there is greenwashing’ – but make no mistake there is a fundamental shift in the finance sector towards net zero, ESG and sustainable finance.

So on the one side you have a big potential for energy efficiency, distributed clean energy, storage, and flexibility services – and on the other side you have a lot of money that wants to invest in this stuff. What is in the middle, what stops capital flowing?

There are many many barriers, particularly for energy efficiency, but the biggest one is the one I call the development gap. That is how do you go from ‘here is a good idea’ to ’here is a quality developed project that can actually be financed and delivered?’. This is a huge gap which has only really been recognized in the recent past, and an area we are beginning to see progress.

One of the things about developing projects, whether it be energy efficiency, renewables, a new wind farm, a new building, or a new car, or a new aeroplane, is that it is risky. You don’t know with certainty what the outcome will be. That development risk requires a different kind of capital to the institutional capital that flows into actual infrastructure projects which is all about achieving low risk and relatively low but safe returns.

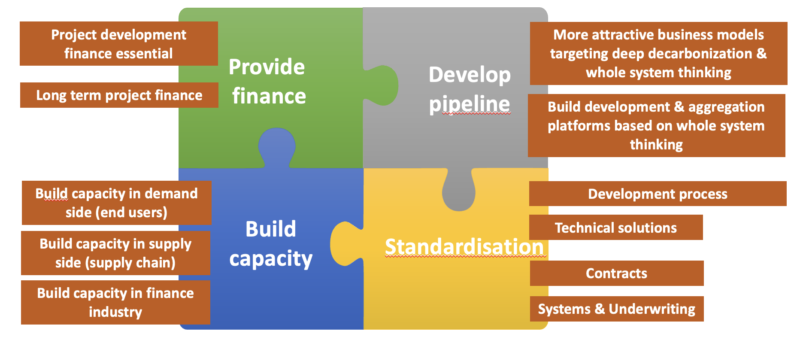

At ep we work globally and we’ve spent the last ten or more years looking around the world at examples where countries or regions have scaled up investment into energy efficiency and decentralised energy and we came up with a simple model – something I call the jigsaw of energy efficiency financing.

There are 4 pieces to the jigsaw:

– Finance – both development and project finance – two very different kinds of capital but both essential

– Pipeline – capital needs to be deployed at scale and so there is a need to build big pipelines by aggregating a lot of small projects. Many of the projects we are talking about are individually tiny by the standards of institutional capital. There is also a need for better business models and business cases that stress multiple benefits to make the proposition more attractive – which helps build pipeline.

– Standardisation – you can only have capital deployed at scale if there is standardisation and that means standardisation of everything, the development process, the technologies, the underwriting processes, the contracts – everything.

– Capacity building – that means for the customers, for the supply chain and for the finance sector.

You can put these four elements together in different ways under different structures – private, public, hybrid, super-ESCOs, procurement frameworks, investment funds. etc. We’ve come to the conclusion that it really does not matter how you put them together but you absolutely need all four to be in the same place at the same time.

One of the ways we are applying this model in real life is the Net Zero Delivery Vehicle. ep has partnered with four local authorities, Essex County Council, Surrey County Council, Kent County Council, and Brighton & Hove City Council and applied for IUK funding to launch the Net Zero Delivery Vehicle, the NZDV. The NZDV will be focused on bridging the development gap. We will see whether our IUK application is successful but if we can get the NZDV funded we think it can develop and deploy c.£100m of capital or more over the next few years.

So in summary:

– We cannot get to net zero without mobilizing private capital at scale

– We need to blend public and private capital

– The biggest need is to fill the development gap

– The development gap is difficult to fill with private capital and is a perfect role for public money to catalyse private investment

– You need all four pieces of the jigsaw to be brought together (USE JIG SAW PROP):

o Finance – development and project

o Pipeline – scale

o Standardisation

o Capacity building for customers, suppliers and finance sector.

Thank you and I look forward to the discussion.

Ironically the event happened at on the day Rishi Sunak announced the watering down of net zero policies. There was a sharp contrast between the leadership being shown by local governments and other organizations, and the lack of leadership being shown by the Prime Minister. I was reminded of a piece I wrote in 2019 (link) and the quote by Ghandi. ‘The future depends on what you do today’.

Following the leaking of the government’s changes in policy I saw that one tabloid had the headline ‘net zero, the tide has turned’ which was clearly an approving headline. Personally it looks to me that the tide is flowing and accelerating – in favour of net zero with more and more investors and organizations, public and private, committing to serious action. Rather than turning the tide the PM is likely to be more like King Canute.

Tuesday 13 June 2023

Last week saw the IEA’s 8th annual energy efficiency conference. The IEA event and the annual energy efficiency market report have helped to advance the energy efficiency agenda, something that for a long time was not given the attention it deserves at policy level.

This transition at the IEA is similar to the UK’s Energy Institute. When I joined the then Institute of Energy, it had grown out of the old Institute of Fuel which was dominated by fossil fuel interests. Beginning in the 1980s and early 1990s, we transitioned the Institute to a more balanced position and included more energy efficiency, as well as renewables on the agenda. Both these institutional changes demonstrate the energy transition in action.

Another indicator of the increasing focus on energy efficiency last week was a capacity building session on energy efficiency financing for banks in AsiaPacific which I presented at. My focus was the Energy Efficiency Financial Institutions Group’s Underwriting Toolkit. This was a tool we authored which provides financial institutions with a framework for assessing value and risk of energy efficiency projects, as well as a common language to ease communication between project developers and financial institutions.

There is no doubt we need to massively scale up investment into energy efficiency. The IEA report shows that global investment into energy efficiency has reached a record $600 billion in 2022, but in order to achieve the net zero scenario this needs to triple to $1,800 billion by 2030.

At ep, our roots are firmly in energy efficiency. The team all have long experience of developing and financing energy efficiency projects, providing advice to companies, investors and governments, and starting and building energy service companies (ESCOs).

We used that experience to develop ESCO-in-a-box®, a licensable business model that enables energy consultants, local energy agencies or equipment vendors to develop high quality bankable energy efficiency projects. It was originally designed in the UK to address SMEs and is now used by five local authorities. We have also adapted it for Kenya, with the support of German aid agency, GIZ where it has been used to develop $20m of projects in a range of sectors. In addition, we are developing it in the Philippines with UN funding.

We are building on these foundations to develop integrated financing vehicles which will build an ecosystem of ESCOs using ESCO-in-a-box®, which in time will be developing a flow of quality, standardised projects, and provide access to finance. Plans are well underway in East Africa and being developed in Asia and India.

ESCO-in-a-box® is an example of how ep works. We invest in small businesses that are supporting the transition to a net zero and regenerative economy, where we can see an opportunity to scale their impact. Then we provide assistance and finance to scale those opportunities, always with a focus on impact. ESCO-in-a-box® also demonstrates another aspect of ep’s work – no one company can do it all and we focus on enabling others.

We need hundreds or thousands of smaller ESCOs all over the world developing and financing energy efficiency projects of all types. The way to get there is to use a proven operating system like ESCO-in-a-box® that builds capacity and enables others to create a viable business.

One of the inspirations for ESCO-in-a-box® was fast food chains, whatever one’s views on their products their operating system enables entrepreneurs, often with little experience, to open and operate a successful business. McDonalds now has 40,000 restaurants world-wide, creating jobs and economic benefits.

We need 40,000 ESCOs world-wide all developing bankable projects to the same standards and delivering them to the sources of capital looking for investments that create real economic, environmental and social benefits – and ESCO-in-a-box® can deliver that.

Find out more about ep Group’s ESCO-in-a-box® model here: https://epgroup.com/what-we-do/consultancy/esco-in-a-box-a-decarbonisation-solution-for-smes/

Thursday 23 February 2023

MITIE asked me to contribute to their 2023 Net Zero Navigator and speak at a breakfast briefing on net zero on the 22nd February. Here are my remarks.

Well here we are at an event looking forward to what may happen in 2023, but we are already more than 10% through the year. It is good to stop and take stock of where we are and where we are going but in the world of energy and infrastructure 12 months is far too short a period. Even with epoch changing events like the invasion of Ukraine, real change happens over much longer periods. And even with events or shocks like that, like the oil shocks of the 1970s or the 2008 global financial crisis, it is only over time that peoples’ thinking changes, organisations change strategy, and ultimately investment decisions are made that shift technologies, infrastructure, and the way we live our lives in a different direction to the one they had been on prior to the change. We can’t really see the effects of those shocks for many years and even decades.

In February 2022, here in the Shard at a MITIE event like this – which was notable as it was the first in person meeting after lockdowns – I made five points which are worth reiterating.

- Net zero is a transition, one that is now driven by investors as much as anyone

- It is not easy – it needs clear leadership and even unreasonableness from business leaders.

- Don’t accept what the vendors are saying – push back and drive new solutions – make them think.

- Think systems rather than components.

- Consider multiple benefits of projects and particularly how they link to the strategic aims of the organisation.

I still stand by those five points and we can discuss them. But when MITIE asked me to think about 2023 and the trends around net zero several other things came to mind and I want to explore them a bit. I am sure that interaction with this audience will help develop the ideas further. I won’t cover all eight of the headlines in the pre-event publicity, just one or two of them, but hopefully you won’t hold that against MITIE.

First of all there is no longer any doubt that we are in the middle of a major energy transition towards renewables. There is still some opposition, particularly from the right-wing nut jobs who think that solar and wind are all about being ‘woke’ and that it will leave us all poorer and living in the cold and the dark. But these people are like the anti-car protestors at the start of the twentieth century who passed laws that said you had to have a man with a red flag walking in front of the car – they will be run over by history and laughed at.

We may also still be having slightly more sensible arguments about the edges of the energy transition, whether or not we should have nuclear power for example or how long do we need gas as a flexible generation source, but we are all clear that there is a global energy transition going on and it is all about decarbonisation, decentralisation and digitisation. We may also have periods when the transition appears to go backwards, for example switching on coal generators because of the effects of the terrible war in Ukraine, but the transition is now unstoppable.

Most of what is written about and spoken about is what I call phase one of the transition and what it seems to me to be happening now is that the emphasis is switching from phase 1 of the transition to phase 2. Energy transition phase 1 is all about energy supply – and mostly power supply – and energy transition phase 2 is all about energy demand.

Phase 1 was all about large-scale centralised power generation. Here in the UK phase 1 really started in 1990 with the introduction of the Non Fossil Fuel Obligation and the first wind farm at Delabole with its 400 kW wind turbines – we have come a long way in 30 years and we now have 13.7 GW of offshore wind operational and 13.7 GW in construction, with a pipeline of 100 GW – a totally amazing achievement – 100 GW is of course more than the total capacity of the grid, and we have offshore wind turbines of 12 to 15 MW each. When I was working on some of the earliest wind farms in 1990/91 such numbers would have been unimaginable which shows that although change is incremental over a year, it is really significant over 3 to 4 decades.

Things are not entirely over yet but it is clear that achieving scale has brought the cost of renewables, particularly solar and wind, down to the point where in most global markets, most of the time, they are the cheapest way of generating power. incumbents will continue to fight back but the writing on the wall is clear. There may be resistance but when it comes to economics ‘resistance is futile’. Of course there will continue to be a role for gas as flexible generation, but even that will come under threat as the cost of storage drops and we perfect other storage technologies other than lithium ion batteries such as liquid air storage and compressed air or hydrogen in salt caverns.

Of course the other big fight in phase 1, which is not yet resolved and is only now getting under way, is all about heat – where things are not so advanced as in power. For domestic heat the incumbent gas industry is still insisting that hydrogen in the gas main and hydrogen boilers are the way to go – this makes no sense at all thermodynamically or economically and is typical incumbent behaviour. The hydrogen industry is very good at employing lobbyists and PR but as Richard Feynman said: “For a successful technology, reality must take precedence over public relations, for nature cannot be fooled”. The future is electric.

And talking about the future being electric – the future of mobility is also electric. There may be situations and limited windows of time where alternative fuels – but not hydrogen – make sense but even large trucks will be electrified. Aviation of course is different but even there, speaking as former pilot and life-long aviation geek, it has been amazing to see how quickly electric aviation has become a thing. It really was still considered impossible ten years ago. Of course, for long haul passenger aviation, which is not going to go away, synthetic aviation fuel is the way to go and great strides are happening in that area.

So if energy transition phase 1 is all about supply of energy, energy transition phase 2 is all about demand, that means that it is focused on the users i.e. you and me, whether that is at the scale of a factory, an office building or an individual home. It is all about the technologies, the behaviours and the organisational and financial structures we employ when we procure and utilise energy.

In 1980 Alvin Toffler, the futurist, coined the word ‘prosumer’ to mean someone who both produces and consumes and to a certain extent it has become a cliché as more and more of us generate our own power through solar PV.

The second word that encapsulates this phase of the energy transition is ’convergence’. This means the bringing together of multiple technologies to produce energy services. In 2020 we worked with EESL, our Indian partner, to develop the convergence business model for India which involves a package of small scale, 1 to 5 MW solar, battery energy storage systems, EV chargers, LEDs, and induction cooking stoves for agricultural communities in India where they now have grid power but it is intermittent. Given that power prices are heavily subsidised in rural India the economic case is a bit different to here in that the Convergence package can provide 24/7 power at a total service cost less than the subsidies that the distribution companies have to pay. There is potential for tens of GW of these systems in India and they are now being deployed.

Why is this example from rural India relevant to our market? Because we have the same trends of cost reduction in solar and batteries and these trends, plus grid constraints and the need to install new infrastructure such as EV chargers, mean that when you do the maths and factor in ancillary services you can supply power at less than grid cost, ensure that it is truly green power, and have long term certainty over power prices – all of which is highly attractive. This convergence model, bringing together local on-site or nearby renewables, batteries and energy efficiency – effectively micro-grids and mini-grids – represents the next big wave of investment.

So what does energy transition phase 2 really mean?

First of all it is clearly based on self-generation – the most you can do given site constraints. This should be PV as far as possible (and increasingly will be) or it could be gas CHP etc. – remember this is a transition – and it can either be on-site or off-site. Secondly it is also about building in flexibility so that means being able to modulate load, up as well as down, which either means modulating equipment of various types and/or storage. Essentially we are moving to the world of Distributed Energy Resources (DERs)and every single piece of energy using equipment, whether it be a motor, a cooling plant, or even a lamp, can become a smart, controllable DER. And every DER can be used to provide energy services to the end user but also back to the grid.

Phase 2 is also about more than just self-generation and changing our energy demand infrastructure. It is also about changing our mental, organisational and financial structures. To take this approach requires a shift in mindset. The traditional mindset is that energy comes out of the cable or the pipe and what we use is simply a function of the technology and the production of whatever we are making or the use of the building – it is an uncontrollable variable. This is a very passive mode whereas what you need in today’s world is an active mode. It means taking responsibility in areas that traditionally you didn’t as an energy consumer. It also requires new capacities and skills within the organisation, or in your suppliers, to design, develop, install and run a set of flexible DERs as part of, or alongside, your basic business process. Essentially you have to become like an asset backed green energy trader – and to get there you have to have a developer mentality.

Phase 2 of the energy transition is also about achieving much higher levels of energy efficiency. My blog is called ‘only eleven percent’ because that is the global level of efficiency from primary energy to useful energy services which is a pretty shocking number. There are still massive opportunities to improve energy efficiency through better management of what we have, and investing with energy efficiency in mind.

Two examples on the former – better management of existing assets. Everybody was going on about the gas crisis because of Ukraine and it turns out that nearly every condensing boiler in the country is set at high flow temperature and therefore not condensing. Simply turning down the flow temperature doesn’t affect comfort and can reduce consumption by 6-8%. Incredible but we let that continue for twenty to thirty years. And an example from schools, where sending out cheap stick on the wall sensors effectively provided a cheap energy management system – lo and behold the data showed the heating was operating all weekend when the school was empty. Basic stuff but still prevalent. You have to get the basics right first before you can consider sensible investment. Then when you do invest there is potential for profitable energy efficiency everywhere.

Every investment should critically examine this potential but usually it doesn’t. We all know that every day investments are being made that lock in higher than needed energy use – either through ignorance, indifference or other pressures. We need to ensure energy efficiency is properly assessed whenever there is any investment that uses or affects energy use. We are working with the Energy Efficiency Financial Institutions Group to help banks and investors operationalise this in what is called the energy efficiency first principle, which is EU policy.

As well as acting more like a hard nosed asset backed energy trader you also have to become more responsible for all the other impacts of your energy use. One really important subject that is rapidly rising up the agenda is biodiversity. Personally I see loss of biodiversity as being more threatening than climate change. We can probably adapt to higher temperatures, albeit at very high high financial and human cost, but if we don’t have any bees left to pollinate crops we are really in a bad way. So how does that link to energy transition phase two? Well let’s say you have the opportunity to build a PV plant, or sign a PPA with one. That is great. You are making a positive impact on the energy transition and adding to clean energy infrastructure. Well done.

But……is it one of those monolithic PV farms that wipes out good land and doesn’t do anything to increase biodiversity i.e. the standard type being offered today? Or is it one that has mixed land use and is designed to positively improve biodiversity? You get to choose. Do you choose greater biodiversity or do you not care and act like the water companies bosses who put profit above all else and think it is ok to discharge sewage into rivers? Just to make the decision more interesting, soon, if not already, the biodiversity enhancing PV farm will become worth more than a conventional one because financial institutions are recognising the need to invest in biodiversity, and will be increasingly required to do so – and guess what, they can’t find enough projects to invest in. So if you are building a PV plant, or even signing a PPA, think about the biodiversity. And what’s more think about the social impact on the community. By the way, none of this is easy but it is important.

The one big thing that has really changed around net zero in the last few years is the pressure from investors of all sorts to implement changes directed towards addressing climate change. I can’t over state this fundamental shift in the investing world, yes you can sceptical and talk about greenwashing and ESG washing – both of which definitely exist – but the pressure is real. It is driven primarily by regulatory and reporting changes such as TCFD, the EU Taxonomy, SFDR and others, as well as risk assessment. Every fund and every investor is affected by these changes, irrespective of any human or moral position they may or may not have, and that pressure is coming down on companies. When the money talks stuff happens.

Every board I sit on or advise is having to react and come up with plans and reporting on net zero. At the top end of companies there is the capacity to deal with it but in the middle range – even within listed companies – and even more in SMEs there is a need for help, the kind of help that my company EP Group provide, or MITIE can provide.

As I said last time I was here – this shift in the financial world gives me optimism as at the end of the day money counts and people tend to do what is needed to get the money.

When we think about changing our infrastructure toward the prosumer and convergence models and financing them we again need to shift mental models. The kind of distributed energy assets we are talking about are too small for traditional infrastructure investors who think in terms of high hundreds of millions if not billions. But a new kind of investor is emerging who sees the potential of funding these kind of projects, not as a one off but as a portfolio, and hundreds of assets across portfolios could reach the scale needed by institutional investors. Some investors are also looking at funding a new type of developer that can develop across technologies in the convergence model.

For big energy users, like the ones we have in the room, they have the portfolios and they have some of the expertise, but they don’t necessarily want to fund the capital – and they probably shouldn’t because it is an infrastructure return and they can get better returns in their core business. To address this imbalance we need new types of partnerships in which customers provide the energy demand – possibly coming together – and infrastructure investors provide the capital through new kinds of energy service providers. We see these new models beginning to emerge.

So to sum up:

- We are now entering phase 2 of the energy transition, a phase in which the focus will be more on localised energy demand than on large scale supply options

- Phase 2 will be about becoming a prosumer and involve convergence of technologies to provide energy services to consumers and the grid

- Phase 2 needs an adjustment in our thinking and taking responsibility for our energy use and supply – and including many other aspects such as biodiversity

- New models of energy services will be funded by infrastructure type investors.

None of this is magically going to happen in 2023 but we clearly see the green shoots of these kinds of developments. As William Gibson said, “the future is here, it is just not evenly distributed yet”. When I play forward ten, twenty or thirty years I think we will see as big a change as we did in energy transition phase 1 from the 1990s to 2023.

And of course I will be happy to discuss these ideas with you now, or in private afterwards. At EP Group we are committed to helping companies and investors think through the options and developing these kind of projects of the future.

Thursday 27 October 2022

An update on ep group’s evolution

At ep group we are best known for our work in energy efficiency, energy services, and the financing of energy efficiency. This work is based on both our experience over many years but also our belief that improving energy efficiency is a critical but still relatively neglected part of the energy transition. We have always been clear, however, that transitioning to a cleaner, more equitable energy system is just one part of the massive challenge we all face in building a more sustainable, and ultimately regenerative economy. Every day, as well as the effects of climate change we see more evidence about the loss of bio-diversity and many other environmental problems such as plastic waste, water pollution etc, problems that affect us all. At the same time, we see social problems such as lack of equal opportunities, as well as poor governance of organisations and countries as being major issues that affect us all and make us poorer in both an economic and a human sense.

![]()

The good news is that there are clear signs of solutions emerging. The rise of interest in stakeholder capitalism, purpose-led companies, impact investing and ESG investing, even allowing for the real problem of ‘ESG washing’, are all positive trends. We see impact investing, investing with an explicit intention to make positive change, along with its corollaries of impact management and impact consuming as the way forward. Our work had always been focused on making a positive environmental impact through improving energy efficiency and when we organised our various companies into ep group we ensured that impact measurement was baked into our operating model. As we were increasingly expanding into other areas we also re-considered our purpose and stated it as follows: ‘to enable maximum impact in the transition to a net zero and regenerative economy in an equitable way’.

It is worth explaining this purpose in more detail. The word ‘enable’ is important as we think maximum impact will be achieved by focusing on enabling many people to have their own impact in their own way, rather than just focusing on our direct impact. This is what Carol Sanford, a leader in regenerative thinking, calls ‘indirect work’. The idea of a ‘net zero’ carbon economy and the need to move towards it to combat climate change is widely understood, but the phrase ‘regenerative economy’ less so. Essentially it means moving investment and resources into systems that restore and regenerate nature, systems that pay attention to quality and well-being and rely on renewable energy flows and the circular economy. The words ‘in an equitable way’ are also vital in this context, much of the modern economy is inequitable, particularly the provision of capital, much of which is extractive, short-term, and not accessible to many people. Being equitable is core to who we are.

![]()

So how are we delivering against our purpose? Our Theory of Change identifies three types of impact we have through our work: increased capacity within organisations to transition to the net zero and regenerative economy; increased investment into net zero and regenerative projects, programmes and companies; and developing and delivering high performance net zero and regenerative projects and programmes in industry and the built environment. Our services, which include: consultancy, research and development; asset management; developing projects; and architecture and design, all contribute to these impacts. Our 2022 impact report, which will be published soon, will summarise some of the impact our work has had across the different businesses.

We have another fundamental belief, and that is mainstream shareholder primacy models of business are clearly part of the problem and that introducing new models of ‘enterprise design’ is a necessary part of the solution in addressing environmental, social and governance problems. Having reviewed different models in use that address the problem, we decided to transition to steward ownership. Steward ownership is based on two principles:

- Self-governance – businesses should be controlled by people working in them.

- Profits serve purpose – profits serve the mission of the company.

Steward ownership will provide a long-term, stable home for the people in the business as well as reward them with a stake in the business.

As well as restructuring we have invested heavily in systems for governance, finance, and impact reporting. Having built our platform the strategy is to scale by agglomeration – bringing into the group other service businesses in adjacent markets that support the transition to a net zero and regenerative economy – and list the company in three to five years. This strategy provides a route to greater value creation and liquidity for business owners, access to cheaper patient capital, the ability to bid for larger projects with large customers, the network effects that can come from working with other parts of the group, and a long-term purpose-led home for their company and their employees.

![]()

Our approach to bringing companies into the group is to first acquire at least 51% of the company in exchange for shares in ep group. The remaining shares will be purchased on an agreed exit multiple after an agreed time, or when the group lists. It is expected that the founder shareholder(s) will stay active in the business for an agreed period but it is not necessary that they should exit completely.

Companies that we bring into the group should:

- be operating in areas that support the Sustainable Development Goals, particularly SDG 7, SDG 9, SDG 11, SDG 12, and SDG 13

- be operating in areas that are complementary to existing ep group

- be EBITDA positive

- have little or no debt

- have founders seeking value realisation within a defined period

- have a complementary culture.

Our offering has proven to be attractive to business owners and we have a pipeline of companies interested in joining the group. It is also attractive to investors, particularly impact investors who cannot normally access the smaller companies which are helping to deliver the transition to a net zero and regenerative economy.

If you are interested in joining us on our journey building a new type of enterprise, or finding out more about the impact-led investment opportunities we have, do get in touch.

Steve Fawkes

Managing Partner

24 October 2022

Dr Steven Fawkes

Welcome to my blog on energy efficiency and energy efficiency financing. The first question people ask is why my blog is called 'only eleven percent' - the answer is here. I look forward to engaging with you!

Get in touch

Email notifications

Receive an email every time something new is posted on the blog

Tag cloud

Black & Veatch Building technologies Caludie Haignere China Climate co-benefits David Cameron E.On EDF EDF Pulse awards Emissions Energy Energy Bill Energy Efficiency Energy Efficiency Mission energy security Environment Europe FERC Finance Fusion Government Henri Proglio innovation Innovation Gateway investment in energy Investor Confidence Project Investors Jevons paradox M&V Management net zero new technology NorthWestern Energy Stakeholders Nuclear Prime Minister RBS renewables Research survey Technology uk energy policy US USA Wind farmsMy latest entries

- The RetroMeter project: using metered energy savings to make energy efficiency more investable

- An overview of the ESCO industry

- Applying Energy Efficiency First in financial institutions

- Getting to grips with the complexities of industrial decarbonisation using soft systems

- Back in Brum – home of the Energy Service Company

- Net Zero: A New Front in the Culture Wars?

- Attracting investment to achieve our net zero ambitions